When Arun finally got his home loan approved, he thought the money would arrive all at once—but at his construction site, the bank officer explained otherwise. As the foundation took shape, the first tranche arrived; when the walls rose, the next followed; and only after the roof and finishing were complete did the final amount come through. Each stage matched the home growing brick by brick, ensuring Arun paid interest only on what he used and the bank stayed confident about progress. By the time he received the keys to his completed house, he realised the staged disbursement wasn’t a delay at all—it was a quiet system working in sync with his dream becoming real.

At a basic level, disbursement stages matter because banks do not simply hand over a large lump sum as soon as your home loan is sanctioned. That would be risky for both the bank and the borrower. Instead, funds are released in tranches (stages), and each stage has clear triggers and checks. The reasons are:

1. Risk Management by the Bank

Releasing money in tranches reduces risk for the bank. If the project halts due to construction delays, legal disputes, contractor issues, or ownership changes, the bank has already released only a portion of funds. This protects the lender against total loss.

2. Aligning Fund Flow with Project Needs

Free-standing homes and custom construction projects often require money at specific points — foundation, plinth, roof slab, finishing, etc. Staged disbursement aligns funds with actual needs so that borrowers don’t pay interest on funds not yet required.

3. Borrower Protection

Staged disbursement protects you from paying interest on the unused portion of the loan. Interest is typically charged only on the amount disbursed — not the full sanctioned amount. If the bank were to disburse everything upfront, you would start paying interest on the entire amount from day one.

4. Quality Control & Verification

At each stage, banks will often check the actual progress — either through technical inspectors, builder certificates, or by comparing contractor bills with completed work — to ensure that funds are used as intended.

5. Regulatory and Compliance Requirements

Banks have to comply with internal and regulatory standards that demand proper monitoring of sanctioned funds. Staged release backed with documentation provides a good audit trail.

In short, staged disbursement balances risk, cost, control, and transparency — for both lenders and borrowers.

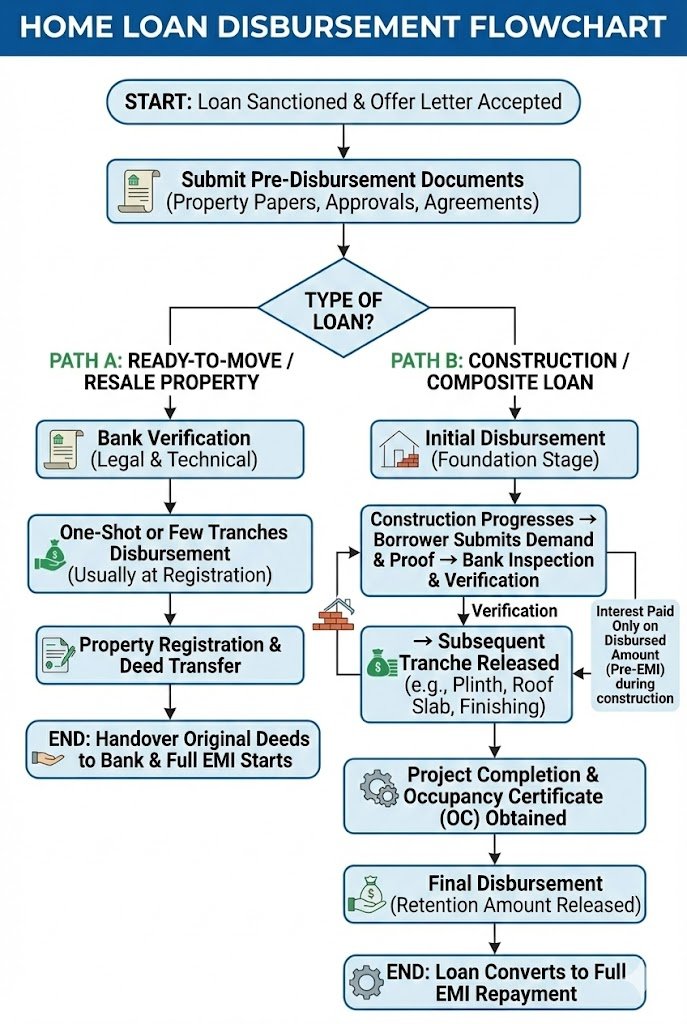

General Disbursement Process – Applicable to Most Home Loans

Before diving into types and specific scenarios, let’s understand the general home loan disbursement flow most banks follow:

Loan Sanctioning

The bank appraises your application and issues a sanction letter that outlines the amount approved, tenure, interest rate, margin (down-payment), and special conditions (if any). You must accept the sanction letter and fulfil pre-disbursement conditions.Submission of Post-Sanction Documents

Banks require key documents before any disbursement. These typically include:

- Original property documents and title deeds

- Building and plan approvals (especially for construction loans)

- Technical estimate, cost breakup, and contractor agreement (for construction)

- Valuation report from the bank’s panel valuer

- Insurance details (fire, home, borrower protections if required)

Satisfaction of Pre-Disbursement Conditions

Some banks may require upfront conditions such as payment of processing fee, legal/technical charges, MODT (Deposit of Title Deeds), or signing of hypothecation agreement.First Disbursement / Initial Tranche

For purchase loans: This could be the entire sale purchase amount.

For construction loans: This is usually a small amount to begin — often called foundation stage disbursement.Subsequent Tranches Based on Milestones

Banks release further funds based on construction progress or legal milestones. These are supported by documentation and inspection reports.Final Disbursement

Once construction is complete and necessary occupancy/ completion certificates are obtained, the bank releases the final tranche.Closure of Loan and Mortgage Creation

Title/ownership transfer and registration formalities are completed at the bank’s office, and the mortgage/hypothecation over the property is created.

This is a simplified overview — each of these steps itself may involve sub-steps and checks in real life.

Disbursement Stages for Ready-to-Move / Purchase Loans

For ready properties (completed houses, apartments, resale properties), the disbursement procedure is simpler compared to construction loans.

Once the loan is sanctioned and pre-disbursement conditions are satisfied, banks usually disburse the entire loan amount in one go to the seller’s account — often tied to the sale deed exchange / registration day. The steps are:

Pre-Registration Disbursement

In many cases, banks transfer the loan amount to the seller just before or on the day of property registration — after confirming legal title, valuation, and clearances.Adjustment at Registration Counter

Sometimes, there’s a small hold (escrow or lender counter authorisation) until registration is completed so that funds are released exactly at the right moment.Balance Adjustments

If you have to pay a remaining portion (down payment or margin money), that must be paid by you before or at the registration counter.Final Documentation at Bank

After registration, the bank collects all original documents and completes internal checks before updating the loan account as disbursed and live.

Key Points for Purchase Loan Disbursement:

• There are usually fewer tranches — often just one or at most two.

• Full amount is released at the point of title transfer / registration.

• You start paying EMI (or interest in some cases) from the date of disbursement.

• No technical inspection reports are typically needed since the property already exists.

Even with purchase loans, banks may hold back a small amount until the original title deeds and registration papers reach their branch.

Disbursement Stages for Construction Loans

Construction loans involve multiple disbursement stages, and this is where staged payments really matter. Construction is often unpredictable — delays, cost overruns, legal checks, contractor issues — anything can happen. For this reason, banks map disbursements to actual physical progress.

A typical construction loan disbursement schedule may include:

1. Foundation Stage Disbursement

This is the first tranche after loan sanction — often a smaller percentage (e.g., 10%–15% of the sanctioned amount). The idea is to enable your contractor to start initial work — excavation, foundation, base reinforcement, etc.

Checklist for This Stage:

• Sanction acceptance

• Down-payment submitted (margin money from your side)

• Building plan approval from local authority

• Architect’s signed cost estimate

• Land title and legal clearances

• Copy of contractor agreement

Banks may insist on seeing the layout plan and structural drawing before releasing this tranche.

2. Plinth Level Disbursement

Once the foundation is complete and visible, the next tranche is released. This is usually verified by either a bank’s technical representative or physically by bank officials.

Key Indicator: Plinth or ground level slab completion.

3. Roof Slab / Super Structure Stage

After the vertical superstructure (walls and roof slab) is significantly complete, the bank releases the next tranche. This is often one of the larger payments because it represents a major milestone.

Verification:

• Bank technical officer inspection

• Contractor bills and receipts

4. Brickwork / Flooring Stage

This tranche is released when internal construction progresses — brickwork, plastering, flooring, etc.

5. Finishing / Fixtures Stage

At or near completion, banks release a large chunk for finishing activities — electrical fixtures, tiling, paint, doors, windows, etc.

6. Final Disbursement / Completion Certificate Stage

Once construction is fully complete and you have necessary occupancy or completion certificates from local authorities, banks release final disbursement. Sometimes banks hold a small retention amount (e.g., 2%–5%) until the original occupancy certificate (OC) is submitted.

What Banks Check at Each Disbursement Stage

Banks usually won’t release the next tranche unless they are satisfied that:

1. Previous Tranche Was Used Appropriately

They may review contractor bills, receipts, material invoices, and even check bank statements of the contractor (if required).

2. Physical Progress Matches Claims

They may send a technical valuer or site inspector (internal or third-party) to verify actual construction progress.

3. No Deviations from Approved Plan

The work must follow the approved architectural plan. Deviations can delay disbursements.

4. Required Approvals and Permissions Exist

At no point should construction violate local rules or lack required approvals (e.g., environmental clearances if applicable).

5. No Legal Issues Have Surfaced

If title disputes, land boundary objections, or encumbrances arise, banks may stop disbursements.

These checks are normal and are in place to protect both you and the bank.

When and How EMIs or Interest Costs Start During Staged Disbursement

One of the most common areas of confusion among borrowers is: “When do I start paying EMIs or interest?”

This depends on how the bank structures your account:

Interest During Construction

During the construction phase, many lenders charge interest only on the amount already disbursed — not on the full sanctioned amount. This is beneficial because interest cost starts small and grows only as more funds are released.

For example, if the sanctioned loan is ₹40 lakh, and you’ve only received ₹10 lakh so far, interest will be charged on ₹10 lakh until the next disbursement.

This type of interest is often called “interest during construction” or “Stage Payment Interest”.

Commencement of EMI

The switch from interest-only payments to full EMIs depends on the lender’s policy. Some banks start EMIs only after final disbursement or completion; others may start EMIs after a fixed period (e.g., 6 months from first disbursement). There may also be a capitalized interest in the final loan amount if interest was paid during construction.

As a borrower, clarify this before signing the agreement.

Disbursement in Plot + Construction Composite Loans

Some banks offer composite loans — where both the plot acquisition and the construction on that plot are financed under a single loan account.

In such cases:

• Initial disbursement is for the plot purchase — often paid directly to the seller at registration.

• After plot transfer is complete, the bank requires submission of the approved construction plan to start staged releases for construction work.

The staged construction release then follows the usual tranche process.

This composite structure is convenient because you don’t have to apply separately for a plot loan and a construction loan — but documentation and staging requirements still apply.

Documentation Checklist for Each Disbursement Stage

Getting your paperwork right is critical. If any document is missing or incorrectly submitted, banks may delay or withhold the tranche.

Common Documents Across Stages

• Loan sanction letter and acceptance

• Copy of approved building plan

• Architect’s cost estimate

• Contractor agreement (if applicable)

• Title deed, encumbrance certificate

• Valuer report from bank’s panel valuer

• Insurance certificates (home, fire, construction risk)

• Receipts and invoices for materials and contractor payments

Documents Specific to Construction Stages

• Photos of work progress

• Technical inspection reports

• Progress certificates from architect or contractor

Documents for Final Disbursement

• Occupancy/Completion Certificate from local authority

• Final contractor bills and receipts

• No-due certificate from architect/contractor

Common Problems and How to Avoid Them

Even seasoned borrowers can make mistakes that delay disbursements. Here are common pitfalls and solutions:

1. Delayed Submission of Documents

If you don’t submit required documents promptly after a milestone, banks can withhold tranches pending documentation. Solution: Always track deadlines and keep extra sets of originals and photocopies ready.

2. Missing or Incomplete Approvals

If the building plan or permissions are incomplete or non-compliant, the bank can refuse fund release. Solution: Get all approvals before applying.

3. Construction Deviations

Changing design, materials, or dimensions without bank-approved revisions can cause delays. Solution: Inform the bank and get approval for any design changes.

4. Contractor Disputes

If the contractor slows work or disputes payment terms, progress stalls — so do funds. Solution: Choose reputable contractors and define clear milestones tied to payments.

5. Unforeseen Legal Issues

Title disputes or government notices can freeze disbursement. Solution: Conduct thorough legal due diligence before loan submission.

How to Plan Your Finances Around Disbursement Stages

Understanding the release schedule helps you plan your personal cash flow:

Keep sufficient margin money available at each funding stage (banks typically finance 75%–90% of project cost, so you must pay the rest).

Anticipate construction delays and the associated carrying cost of interest.

Set aside funds for pre-disbursement costs like processing fees, insurance, technical/legal charges.

If a bank releases disbursements slowly, you may have to advance funds from your savings or credit until the bank reimburses. Planning helps avoid cash crunches.

Disbursement stages are a foundational element of home loans, especially in construction and plot financing. Banks structure tranches to ensure:

• Funds are used responsibly

• Interest cost is minimized for borrowers

• Project milestones are aligned with releases

• Documentation and compliance are maintained

For borrowers in Tamil Nadu or anywhere else in India, recognizing the logic behind staged disbursement helps you negotiate better, anticipate cash flows, and avoid project delays. Whether you are dealing with SBI, HDFC, Canara Bank, Axis, or a housing finance company, the principles remain the same — clarity, documentation, compliance, and communication are key to smooth and timely disbursements.

By following the tips, checks, and process flows described above, you’ll be equipped to manage home loan disbursement like an expert — protecting your interests and ensuring your dream home gets built on time, without financial surprises.